Confused by Furnished Holiday Let Capital Allowances in 2026? Learn how to maximize tax relief for your Brighton holiday home and navigate the new HMRC rules to keep your holiday let profitable.

The rulebook for self-catering properties just went through its biggest rewrite in forty years.

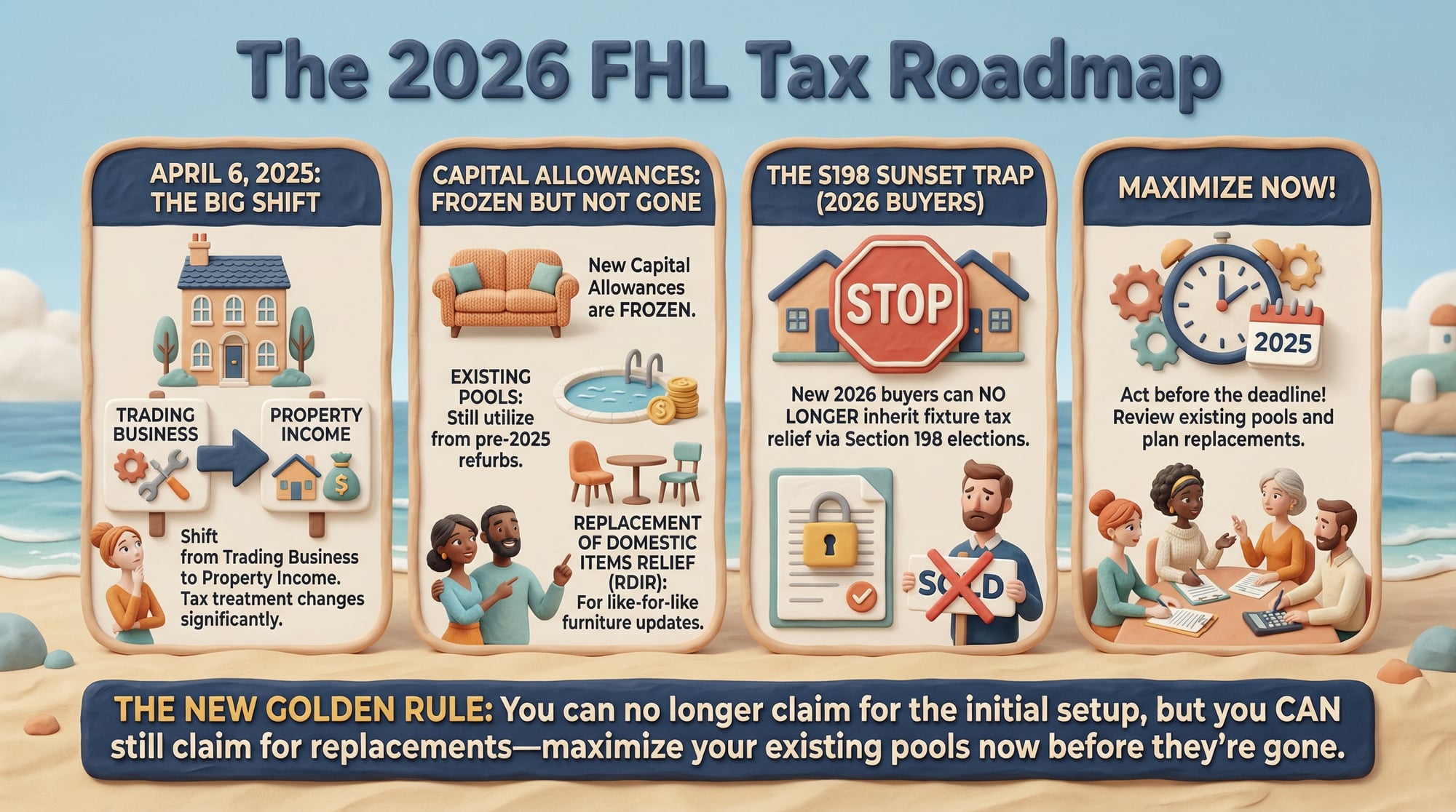

As of 6 April 2025, the government abolished the Furnished Holiday Let (FHL) tax regime.

If you're looking at your 2026 tax return and wondering if those valuable capital allowances have vanished into the sea mist, the answer is: mostly, but not entirely.

The Big Shift: Trading vs Investment

For decades, HMRC viewed your Brighton holiday let as a "trading business," similar to a hotel. This meant you could claim capital allowances on almost everything inside the property, from the sofa to the entire heating system.

Since the rules changed, most short-term lets are now treated as “property income businesses,” the same as standard buy-to-lets. This means you generally can’t claim capital allowances on new purchases made after April 2025, unless the expenditure relates to non-residential areas such as shared facilities in a mixed-use building.

What You Can Still Claim in 2026

While the "new spend" door has closed, there are two important ways you can still find tax relief for your property's contents:

Existing "Pools": If you already had a capital allowance claim running before April 2025, you don't lose it. You can continue to claim writing-down allowances on your existing pool until it's completely used up. This is great news for anyone who did a major refurb in 2024.

Replacement of Domestic Items Relief (RDIR): This is your new best friend. While you can't get relief for the initial cost of furnishing a property anymore, you can deduct the net cost of replacing items like-for-like under the Replacement of Domestic Items Relief. This covers furniture, furnishings, carpets, and white goods, provided the replacement is equivalent and not an improvement.

The "S198 Sunset Trap" for New Buyers

If you're planning to buy a holiday let in Brighton during 2026, the landscape is very different. Previously, a buyer and seller could sign a Section 198 election to fix the value of "fixtures" (like kitchens and electrical systems) and pass the tax relief to the new owner.

Because holiday lets are now classed as dwelling-houses in this respect, you can no longer use Section 198 elections.

In plain English: if you buy a property in 2026, you generally won't be able to inherit any capital allowances from the seller, even if they had a valid claim running.

Action Plan for 2026

If you're operating a holiday let this year:

Audit your assets: Check if you have an unclaimed "pool" of allowances from before April 2025. You may still be able to amend your 2024/25 return until 31 January 2027. Speak to a Capital Allowances specialist such as Zeal to see if you can make a claim.

Track every replacement: Keep meticulous digital records of any furniture or appliances you replace this year to use the RDIR relief.

Speak to a Capital Allowances specialist like Zeal for tax planning and advice.